Many people search for the difference between Roth and 401(k) because retirement planning can feel confusing, especially when tax rules and investment accounts are involved.

Beginners often hear terms like Roth IRA, Roth 401(k), traditional 401(k), employer match, and tax free withdrawals without fully understanding how these retirement options work.

In simple words, a Roth account uses after tax money with tax free withdrawals in retirement, while a traditional 401(k) usually uses pre tax contributions that are taxed later during retirement withdrawals.

The difference between Roth and 401(k) becomes important when planning long term savings, retirement income, taxes, investment growth, and financial flexibility.

This guide explains Roth and 401(k) clearly, including definitions, taxes, contribution rules, employer matching, withdrawal rules, similarities, real world examples, and expert retirement planning insights.

Quick Answer: Difference Between Roth and 401(k)

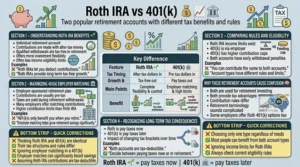

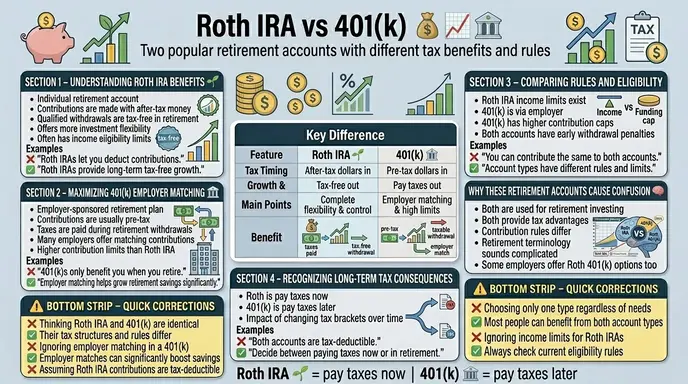

The main difference between Roth and 401(k) is when taxes are paid on retirement contributions and withdrawals.

- Roth accounts use money that has already been taxed, allowing tax free retirement withdrawals

- Traditional 401(k) accounts usually reduce taxable income now, but withdrawals are taxed later in retirement

For example:

If you contribute to a Roth account today, you pay taxes now. If you contribute to a traditional 401(k), taxes are usually paid when you withdraw the money later.

Definition of Roth and 401(k)

- Roth: A retirement savings account funded with after tax income, allowing qualified tax free withdrawals later.

- 401(k): An employer sponsored retirement plan that usually allows pre tax contributions and tax deferred growth.

Simple Example

- Roth = pay taxes now, withdraw tax free later

- 401(k) = save taxes now, pay taxes later

Pronunciation of Both (US & UK)

| Term | US Pronunciation | UK Pronunciation |

| Roth | rawth | roth |

| 401(k) | four oh one kay | four oh one kay |

Now let’s understand this clearly through taxes, investing, employer plans, and retirement income strategies.

Difference Between Roth and 401(k) Comparison Table

| Feature | Roth | Traditional 401(k) | Similarity |

| Tax Timing | Taxes paid now | Taxes paid later | Both help retirement savings |

| Contribution Type | After tax money | Usually pre tax money | Both allow investing |

| Withdrawal Taxes | Usually tax free | Usually taxable | Both have retirement rules |

| Employer Sponsorship | Often individual account | Employer sponsored plan | Both support long term growth |

| Taxable Income Today | No deduction usually | Reduces taxable income | Both provide financial planning benefits |

| Retirement Flexibility | Tax free withdrawals | Tax managed withdrawals | Both build retirement wealth |

| Investment Growth | Tax free growth potential | Tax deferred growth | Both can hold investments |

| Required Withdrawals | Roth IRA has fewer lifetime requirements | Traditional 401(k) has required withdrawals | Both regulated by tax law |

This table clearly shows the difference and similarity between Roth and 401(k) for quick understanding.

Key Differences Explained Between Roth and 401(k)

Tax Timing Difference

The biggest difference involves taxes.

- Roth = taxes now

- Traditional 401(k) = taxes later

This affects long term retirement planning significantly.

Tax Free Retirement Withdrawals

Qualified Roth withdrawals are generally tax free.

Retirement\ Withdrawal\ Tax_{Roth}=0

This simplified expression reflects how qualified Roth withdrawals may avoid income taxes.

Traditional 401(k) withdrawals are usually taxed as ordinary income.

Employer Involvement

Traditional 401(k) plans are commonly offered by employers.

Many employers also provide:

- Matching contributions

- Automatic payroll deductions

Contribution Flexibility

Roth accounts may have:

- Income limits

- Different annual contribution rules

401(k) plans often allow higher contribution limits.

Retirement Tax Strategy

People expecting higher future tax rates may prefer Roth accounts.

People wanting lower taxes today may prefer traditional 401(k) contributions.

Why Do Roth and 401(k) Accounts Exist?

Governments encourage retirement savings by offering tax advantages. Different retirement accounts exist because people have different income levels, tax strategies, career situations, and retirement goals.

Some savers prefer immediate tax savings, while others prefer tax free retirement income later.

How a Roth Account Works

After Tax Contributions

You contribute money after paying income taxes.

Tax Free Growth

Investments inside the account can grow without future qualified tax obligations.

Retirement Withdrawals

Qualified withdrawals are generally tax free if rules are met.

Popular Roth Investments

Roth accounts often include:

- Stocks

- ETFs

- Mutual funds

- Index funds

Investment platforms from Vanguard and Fidelity Investments commonly support Roth retirement accounts.

How a Traditional 401(k) Works

Pre Tax Contributions

Money is deducted from paychecks before taxes in most traditional 401(k) plans.

Lower Current Taxable Income

Contributions may reduce taxable income today.

Taxable\ Income = Salary 401(k)\ Contribution

This simplified relationship shows how contributions can lower current taxable income.

Taxed Retirement Withdrawals

Withdrawals during retirement are usually taxed as income.

Employer Matching

Many employers match part of employee contributions, which can significantly increase retirement savings over time.

Difference Between Roth and 401(k) in Real Life

| Real Life Situation | Roth | Traditional 401(k) |

| Young workers | Often attractive | Also useful |

| High earners today | Sometimes less attractive | Often preferred for tax reduction |

| Retirement tax planning | Strong tax free benefit | Strong upfront tax benefit |

| Employer matching | Usually separate | Common feature |

| Flexible retirement income | Higher flexibility | Taxable withdrawal planning needed |

Many people use both account types together.

Difference Between Roth and 401(k) for Beginners

Roth Advantages for Beginners

Younger investors often choose Roth accounts because:

- They may currently be in lower tax brackets

- Long term tax free growth can become valuable

401(k) Advantages for Employees

401(k) plans are popular because:

- Payroll deductions are automatic

- Employer matching can boost savings quickly

Diversified Tax Strategy

Financial advisors often recommend mixing taxable and tax free retirement income sources.

Real Life Examples with Roth and 401(k)

Early Career Worker

A younger employee expecting higher future earnings may prioritize Roth contributions.

High Income Professional

Someone seeking immediate tax reduction may favor traditional 401(k) contributions.

Employer Matching Scenario

If an employer matches contributions, participating in a 401(k) can provide valuable additional retirement savings.

Retirement Flexibility

Retirees using Roth accounts may manage taxable income more efficiently during retirement years.

Financial Planning Platforms

Companies like Charles Schwab and Fidelity Investments provide tools for comparing retirement strategies and investment growth projections.

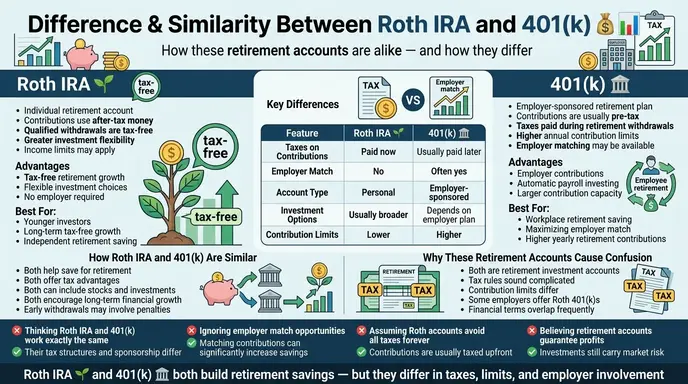

Difference + Similarity Between Roth and 401(k)

| Feature | Roth | Traditional 401(k) | Similarity |

| Tax Benefit Timing | Later | Now | Both provide tax advantages |

| Contribution Style | After tax | Pre tax usually | Both build retirement savings |

| Investment Options | Wide variety | Wide variety | Both support long term investing |

| Retirement Goal | Tax free income | Deferred taxes | Both help future financial security |

| Employer Role | Limited | Commonly employer sponsored | Both regulated retirement accounts |

| Financial Planning Use | Long term tax planning | Immediate tax planning | Both useful for retirement |

This table clearly shows the difference and similarity between Roth and 401(k) for quick understanding.

Why People Get Confused Between Roth and 401(k)

Similar Retirement Purpose

Both accounts help people save for retirement.

Multiple Account Types

People often confuse:

- Roth IRA

- Roth 401(k)

- Traditional IRA

- Traditional 401(k)

Tax Complexity

Retirement tax rules can feel complicated for beginners.

Financial Industry Terminology

Financial advisors and media frequently use technical language that overwhelms new investors.

Common Mistakes with Roth and 401(k)

| Mistake | Correct Understanding |

| Thinking Roth means tax free contributions | Taxes are paid before contributing |

| Assuming all 401(k) plans are tax free later | Traditional withdrawals are taxable |

| Ignoring employer match benefits | Employer matches can be valuable |

| Believing only one account can be used | Many people use both |

| Forgetting withdrawal rules | Retirement accounts have regulations |

Quick Memory Tip

- Roth = taxed now

- Traditional 401(k) = taxed later

When to Choose Roth or 401(k)

Choose Roth When:

- You expect higher future taxes

- You want tax free retirement withdrawals

- You are early in your career

- Long term growth matters most

Choose Traditional 401(k) When:

- You want lower taxes today

- Your employer offers matching

- You currently earn a high income

- You expect lower taxes in retirement

Many financial planners recommend combining both for tax diversification.

Expert Insight

In real retirement planning, the best choice often depends less on the account itself and more on future tax expectations, income growth, and long term financial strategy.

Roth accounts can become extremely valuable for younger investors because decades of tax free growth may outweigh the benefit of today’s tax deduction.

Meanwhile, traditional 401(k) plans remain powerful because employer matching effectively adds extra retirement money many workers would otherwise miss.

For many households, using both account types creates flexibility by balancing taxable and tax free retirement income later in life.

Modern retirement planning increasingly focuses on diversification not only in investments, but also in tax exposure during retirement.

Frequently Asked Questions

What is the main difference between Roth and 401(k)?

Roth accounts are taxed now, while traditional 401(k) accounts are usually taxed during retirement withdrawals.

Is a Roth better than a 401(k)?

It depends on income, taxes, employer benefits, and retirement goals.

Do employers match Roth accounts?

Employers commonly match 401(k) contributions, though some plans include Roth 401(k) options.

Are Roth withdrawals tax free?

Qualified Roth withdrawals are generally tax free.

Can you have both a Roth and a 401(k)?

Yes. Many people contribute to both.

Which account lowers taxes today?

Traditional 401(k) contributions usually lower current taxable income.

Is a Roth good for younger workers?

Often yes, because future tax free growth may become valuable over time.

Why do financial advisors recommend diversification?

Different account types provide flexibility for future tax planning.

Conclusion

Understanding the difference between Roth and 401(k) helps people make smarter retirement and tax planning decisions.

Roth accounts use after tax contributions and offer potential tax free withdrawals later, while traditional 401(k) plans usually provide upfront tax advantages with taxes paid during retirement withdrawals.

Both account types offer powerful retirement savings benefits, but they serve different financial goals and tax strategies.

Roth accounts may benefit younger workers expecting higher future earnings, while traditional 401(k) plans remain highly valuable for reducing taxable income today and taking advantage of employer matching programs.

In real world financial planning, many investors use both options together to create long term flexibility, balanced tax exposure, and diversified retirement income.

Once you fully understand the difference between Roth and 401(k), retirement planning becomes far less confusing and much easier to manage confidently.

Discover More Articles!

Difference Between Diamond and Moissanite:With Examples

Difference Between Zucchini and Squash:With Examples

James Whitmore. Labdiff.com is my english grammar comparision website. I explore the history and evolution of English words. I write detailed comparisons explaining why spellings change over time and how British and American English diverged. My articles add depth and credibility to grammar comparison topics.